{kind=link}

Subscribe to Point Me Awake, a morning jolt of the top stories in travel every Monday, Wednesday, and Friday — straight to your inbox. Our curated list includes deals, reviews, and the best ways to use points and miles.

I get questions all the time from friends and colleagues regarding the credit card aspects of life — and not just from my travel hobby enthusiasts.

One of the biggest conversations also revolves around credit scores. People argue that using credit helps, others say that not using their cards improves their scores. The other day, I had a vigorous discussion surrounding the issue of how cancelling a credit card account affects your credit score.

With over 24 credit cards, I find it necessary to close one or two every now and then. I am not a churner of credit cards although many people use this strategy for rewards and points building.

While credit scores are based on a number of factors, keeping an older account potentially can help your credit score. The decision to close accounts should be based on a matrix of factors, such as if there is an annual fee, what are the benefits to the card, and if the card affects your ability to get other cards (within that bank’s portfolio or not).

How Is Your Credit Score Calculated?

Before we delve into the answer to the question of whether closing an account hurts your credit score, we need to understand how these scores are determined.

(Image by CafeCredit)

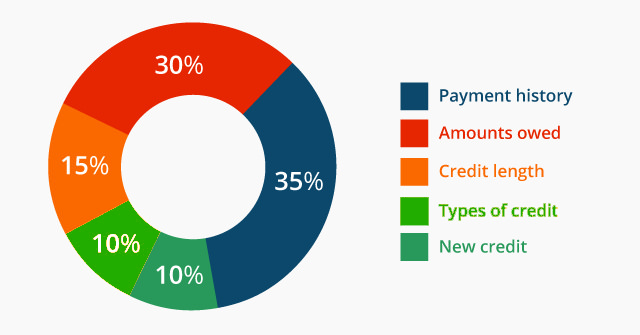

Your credit score is weighted according to the following components:

- 35% of your score is your payment history (a percentage of payments you have completed on-time)

- 30% of your score represents your credit utilization (how much credit you have in comparison to the total limits of your accounts)

- 15% of your score is your credit length (the average length of your open accounts)

- 10% of your score is the types of credit you use (how many diverse types of requests for credit you have)

- 10% of your score is your requests for new credit (how many times you have applied for credit)

To highlight the big points: what’s most important is you (1) do not have too much of your credit tied up, (2) you limit your available credit, (3) you make on-time payments, and (4) your average length of accounts is relatively long.

Logically, if you have an older account (credit length) that you are considering closing, it likely does not have a balance or perhaps it’s very low (credit utilization.) So the low balance and the age of the account would be positively impacting your credit score.

The payment history will still be a part of your credit score even if you close that account.

So How Could Closing An Account Hurt You?

To illustrate this point (in an extreme example), let’s say a person has only two credit cards. Each card has a limit of $5,000 and this person spends only a total of $4,000 per month on charges, but pays these charges off each billing cycle.

Card A has been open for less than a year and card B has been open for 10 years.

At this time, the credit score would probably look good. Credit utilization of 40% ($4,000 spent and $10,000 limit). Credit length would an average of say 5.5 years.

Say this person feels that card B wasn’t rewarding enough and card A is a better choice for their monthly spend. If this person closed card B (held for 10 years), we would expect the credit score to drop significantly. Credit utilization would increase to 80%. (Although by paying off the card’s balance before the due date, that number could be zero. Credit utilization is calculated on the due dates.) Credit length would only a year.

In the short term, this person would be better off using card A, which provides travel rewards, and keeping card B open just to keep their credit score up. But this person also needs to look at a long-term approach to get them more rewarding credit cards.

When Closing a Credit Card Might Not Hurt Your Credit Score

Now let’s use an example at the other end of the spectrum:

- A person has 20 or more credit cards

- Credit utilization is kept low (either low usage or paying the bills before the statement due dates)

- This person’s average credit length is 8 years

In this person’s scenario, if they were to close one of the newer cards, we wouldn’t expect it to have a negative impact on their credit score. That’s because their credit utilization is so low that it wouldn’t materially change.

How to Reduce the Impact of Closing Credit Cards

So I am not saying that you should never close a credit card. Applying for and getting reward cards with big sign-up bonuses is a huge part of the travel landscape today. With so many lucrative offers, you are bound to get new cards and close others.

A few things to consider would be that if you want to keep higher credit length numbers, you should consider no annual fee credit cards. That way, the age of credit can increase over time, helping raise your credit score, without costing you in fees to do so.

Consider these steps:

- Perhaps you have a card you have held for a long time, closing would ding your credit score. Consider seeing if there is an option to downgrade the card to a similar no-fee product.

- If you have not been doing so, try using the credit utilization tip I told you about earlier (paying off balances before the due date which you should be doing anyway) to lower that number and raise your credit score.

- Keep those no-annual fee cards that improve your credit score over time. You will find there are a few who also offer travel rewards

The Upshot

Regardless of your portfolio of credit cards, I find there’s so much value in acquiring and keeping long-term no annual fee cards that are at least somewhat rewarding. A couple of great no-fee options are the Chase Freedom Unlimited and Chase Freedom. Those two can help maintain your credit score over the long term when downgrading from a more premium card (like the Chase Sapphire Reserve).

In fact, the Chase Freedom Unlimited currently offers 3% cash back on your first $20,000 spent on purchases in your first year and 1.5% thereafter. Not a bad return for a no annual fee card.

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.