{kind=link}

My parents and sister are pretty good sports when it comes to credit cards, essentially applying for whatever I tell them to. However, I guess I neglected my duties on the backend, not reminding them to let me know when the annual fees were coming due besides my initial instructions upon application. The day after Thanksgiving I had them lay all their current credit cards across the kitchen table…it was a disaster. Way too many cards (I took a few great pictures but for security reasons they aren’t posted here) and surely some that seemed a bit too old to not have the annual fee charged or coming up. So here’s what we did:

Step 1 – Separated cards by issuer.

Step 2 – Logged in to the online accounts to check on the annual fees

Step 2B – Wait, unknown user names and / or passwords for most cards

Step 2C – Wait, multiple Chase cards with different logins that needed to be combined into one account. We combined both personal and business into one online account.

Step 3- Phew, the only annual fees charged were within the last 60 days. The plan was to send a message to the secure message center to cancel the cards and reverse the fees…but first we needed to leverage those credit lines and transfer them to some new cards…or at least use them as leverage with the reconsideration lines!

Step 4 – Apply for the new cards (see the details below)

Step 5 – Once we received the approvals, I went back and emailed each bank to cancel the old cards, refund the fees (if charged), and move the remaining credit lines over (some had already been adjusted to win approval for the new cards).

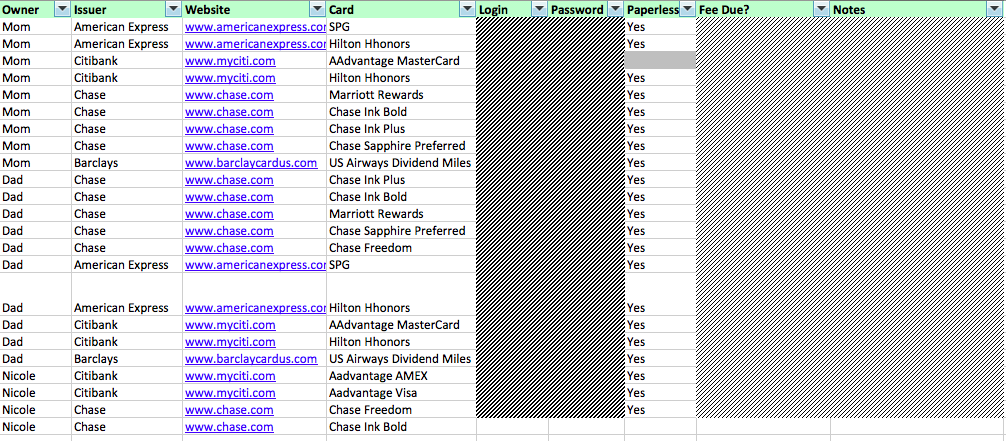

Step 6 – DOCUMENT DOCUMENT DOCUMENT. I created an Excel sheet listing the current cards, the issuer, the online website, the product, the login and password, whether we set up paperless statements or not, any annual fee dates, and some relevant notes. Here’s a snapchat of what the sheet looked like about half way through the process…

Step 7 – Spending instructions so that they know when to use each card (see the bottom of the post).

Card Details – I essentially used the same cards from my last App-O-Rama:

Chase Ink Plus® Business – Why? Last December both my parents were issued the standard at the time which was a MasterCard. Now, there were rumblings in early September that the Ink Plus as well as the Ink Bold were being issued as Visas…very exciting news! A Visa is actually a lot more useful for me due to my travel patterns so I went ahead and applied. After speaking with Chase and foregoing the current Ink Plus MasterCard, my mom was approved. Strangely enough, the same approach did not work for my Dad as he had too many recent Chase cards and too many recent requests for credit…though my Mom and I have the exact same history in terms of applications and Chase cards and similar credit scores. Anyway, my Mom will receive 50,000 Ultimate Rewards points after spending $5,000 within three months, annual fee waived for the first year. I’ve personally found it easier to obtain approval for the Chase Ink Plus cards, as they are credit cards as opposed to the Chase Ink Bold which is a charge card. A credit card allows you to pay part of your bill each month while a charge card requires you to pay your balance in full. Issuers tend to look for higher credit scores for charge cards.

Citi Business MasterCard – Why? It’s been well over the recommended (and required) 65 day wait since applying for their personal Citi AAdvantage cards and why not get another 50,000 AAdvantage miles after spending $3,000 within three months. Annual fee waived for the first year. Automated approval for one parent and call required for the other. In the end, both approved.

Chase Freedom® – $200 Bonus Cash Back – Why? Two reasons really. For a limited time, Chase has doubled the offer on the card from 10,000 points to 20,000 Ultimate Rewards points, after spending $500 within three months with no annual fee! Additionally, my Mom didn’t have the Visa edition of the Freedom card. No Longer Available for the increased bonus.

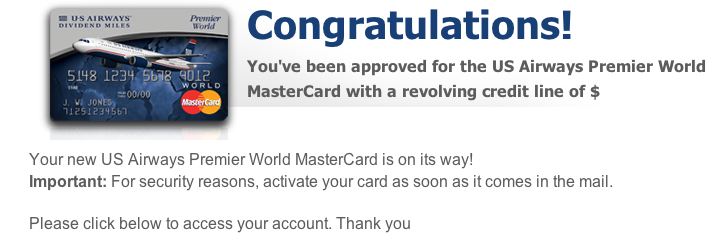

The US Airways® Premier World MasterCard® – Limited Time Increased Offer!

With the pending AA/US merger this card is a must as these miles will one day become AAdvantage miles. This card will eventually go away, leaving behind the harder to obtain AA Citi Cards. While Barclays is one of the tougher banks in terms of approval for your first card, they have a reputation lately as being easy to obtain additional cards. This one was very important to me. After receiving the sign-up bonus and then an additional 15K bonus on my last US card, I wanted to apply for another non business version of the card. Automated APPROVAL! Here’s hoping the 15K additional bonus now returns for this card as well. Current best offer (updated 4/30/14). 40,000 bonus miles after first purchase and payment of the $89 annual fee. That’s 30,000 40,000 more AAdvantage miles for me (or perhaps a fuel surcharge free BA ticket)! See Building Up US Miles for the AA Merger – Time to Take AAdvantage, Full List of Offers!

1) 40K 30K after your first purchase, annual fee of $89, up to an additional 10k when you transfer a balance within 90 days (1 mile per $). Full landing page and promo details.

- Earn 40,000 bonus miles after your first purchase and payment of the $89 annual fee*

- First checked bag free on eligible bags for you and up to four companions on domestic US Airways operated flights

- One companion certificate good for up to 2 guests to travel with you on a US Airways operated flight at $99 each, plus taxes and fees

- Priority boarding Zone 2 on US Airways operated flights

- Redeem miles for award travel on US Airways and American Airlines booked through usairways.com or US Airways Reservations

- Earn miles on every purchase with 2 miles for every $1 you spend on US Airways purchases and 1 mile for every $1 on purchases everywhere else

- Please see terms and conditions for complete details

Club Carlson Premier Rewards Visa Signature Card – Did this one for Dad. Up to 85,000 points (50K after the fist purchase and 35K more after spending $2,500 within 90 days). You’ll also receive complimentary Gold status and the awesome benefit that makes the second night of any award stay free! I didn’t jump on this card when it first came out (just b/c I was busy traveling), but it was certainly nice to have another non Chase / AMEX card to have them apply for! Auto approved (note I did this card first due to US Bank’s intense credit review followed directly by the Barclays app). Automated approval as this is their one and only US Bank card. Not as lucky? Consider 1-800-947-1444 or 1-800-685-7680.

Barclaycard Arrival Plus™ World Elite MasterCard® – Also for Dad. I sat out on the hype over this card when it was first released and I’m still not sure why everyone is going so crazy over it. I understand the benefits -double points on all purchases / no worrying about category spend, waived annual fee first year, free subscription to TripIt, and a free copy of your FICO score. More importantly, no worrying about award availability as you are actually buying a ticket with your points. The points are valued at 1.1 cents per mile when redeemed for travel and you receive a statement credit for their value. Since you are buying the ticket, you’ll actually be earning miles on your award ticket. That’s all great but I sign up for these cards to fly in business / first to international destinations, quite difficult to achieve when my points are only worth 1.1 cents. So why did I apply? Incidental travel costs, positioning flights for mileage runs, and some potential domestic trips that I don’t want to burn my valuable airline miles on. Little known fact, you can actually redeem the miles for anything labeled “travel” on your statement and so that means they are great for seat upgrades, rental cars, club memberships, etc (more useful with my parents for their travel patterns). When you apply you’ll receive 40,000 points (which equals $440 when redeemed for travel).

PS – you may also want to consider the Chase Sapphire Preferred which also has a limited time increased sign-up bonus. See Chase Sapphire Preferred Limited Time Point Offer Increase!

Spending Instructions for Mom

You currently have a Starwood AMEX (card and offer expired), Hilton AMEX, Citi AAdvantage, Citi Hilton, Chase Ink Bold, Chase Freedom MasterCard, and Chase Sapphire Preferred .

In the mail are coming the new Chase Ink Plus, Citi Business AAdvantage, Chase Freedom Visa, and another US Airways card.

Here’s how you should spend:

- Make one purchase on your Barclays US Airways card, then put it in the drawer. There is NO minimum to get the points so use it once on something small, then put it in the drawer.

- Hit the spend requirements on the Chase Ink Plus, Citi Business AAdvantage, and Chase Freedom. Use the Vanilla Reloads from CVS as discussed. Once completed put the Citi Business in the drawer.

- Chase Sapphire Preferred for all dining (restaurants, bagel store, etc.)

- Chase Sapphire Preferred for all travel (train, taxi, hotel)

- Chase Ink Plus (office supply stores, internet, cable, cell phone)

- Starwood AMEX everything else (groceries, clothing, CVS, etc.)

- Chase Freedom – On rotating categories each quarter (see https://creditcards.chase.com/freedom/calendarreminder). This quarter Oct-Dec is 5x points on Amazon and department stores.

ENJOY – Love Ya!

Dad got a similar list and both my parents printed out their emailed list and are already referring to the spend guidelines…such good students!

Anyone else have some family points fun over the Thanksgiving holiday?

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

8 comments

My last app day involved, in this order: 1) $0 Barclay Arrival ($440); 2) $395 Ritz-Carlton ($200 Ritz card + $200 ’13 airline credit + $200 ’14 airline credit + 70,000 Marriott points & Gold status); 3) $0 Citi AA (50,000 AAdvantage); 4) $75 BofA Air Alaska ($100 statement credit + 25,000 Alaska).

There are no spending instructions for Barclay arrival card. Where does that fit in?

He mentioned Barclay’s $1 min spend.

You make your parents do Vanilla Reloads?

You have your *parents* buying Vanilla Reloads? Are you insane? Seriously, I do this myself but consider it a bit burdensome/taxing/time consuming/advanced. I certainly don’t have my wife participate. Seems a bit off the rails…

Great post! I had to laugh because in my family, my husband is the one who has to be reminded about which card to use for each purchase. I drive him a little crazy with this stuff, but he loves the rewards.

Great post. Nice excel sheet. That’s my saving grace as well although another important column I include is whether full auto pay is on for my cards. With 36 active cards between me and my wife, I’d be doomed without autopay.

My parents passed away awhile back but I’m sure I would have attempted to have them join my churning cult as well. Knowing them they would have thought I was insane. Getting the wife to call reconsideration is like going to hell and back, despite the fact every time she does, she gets approved because of her calm demeanor – that is calm after the storm of chewing me out for making her call. Of course she digs the free vacations so she complies like instructed :). My son is only 10 but I’m already thinking ahead for him. I need serious help.

@Kent C – Love it!!! Your son will be ready soon 😉

Sorry but I just feel it’s too off and maybe a little too greedy too. Maybe this is why this country is going downhill….